CBDC, or central bank digital currency, is a digital form of fiat money issued and backed by a country’s central bank. Unlike cryptocurrencies, CBDC is centralized and regulated by the government, and is meant to function as a digital version of traditional fiat money. Although the application of CBDC is still in its infancy, some nations are investigating the potential benefits and drawbacks of doing so.

The blog explains the Central Bank Digital Currency (CBDC) in detail. It covers what CBDC is, how CBDC works, its different types, its benefits, and what the future of CBDC will be. The blog provides an extensive outline of CBDC.

What is CBDC – Central Bank Digital Currency?

Digital forms of currency issued by central banks are known as central bank digital currencies (CBDCs). They are designed to provide a secure and convenient alternative to physical cash and to facilitate digital payments for individuals and businesses.

CBDCs are backed by the central bank, which means they have the same value as traditional fiat currencies and can be used in the same way. Dissimilar to digital forms of money, which are not managed by a central authority, CBDCs are issued and controlled by the central bank.

Some instances of central banks that have issued CBDCs include the Federal Reserve in the United States and the Bank of England in the United Kingdom.

- A digital form of money issued by a central bank is known as central bank digital currency (CBDC).

- The central bank directs and regulates it.

- CBDC depends on a computerized record and could conceivably utilize blockchain or distributed ledger technology.

- The supply and value of CBDCs are influenced by a country’s monetary policies and trade surpluses.

Compelling Facts & Stats of Central Bank Digital Currency

- According to a report, by 2023, more than 20 countries will take significant steps to pilot a CBDC. India, Australia, Brazil, Thailand, South Korea, and Russia intend to continue or start pilot testing in 2023.

- CBDC will raise significant privacy concerns.

- According to the resources, approximately 90 percent of the world’s central banks are pursuing central bank digital currency (CBDC) projects.

- The future of the central bank digital currency is related to the future of networks.

- As per Statista, more and more countries are preparing to jump on board a different crypto hype bandwagon.

How Does Central Bank Digital Currency Work?

A digital version of a nation’s fiat currency known as a CBDC is issued and backed by the central bank. It works similarly to physical money and can be used for transactions, such as paying employees or purchasing goods and services. Many countries are currently developing their own CBDCs, which may have different features and functions, but all follow the same general concept.

CBDCs are similar to existing digital payment methods in that they allow money to be transferred between accounts digitally. Unlike traditional digital payments, however, CBDCs would not have to go through multiple banks, which can take several business days. Instead, transactions could be completed almost instantly on a single digital ledger.

Furthermore, consumers would not need to have a business bank account to use a CBDC, which could be beneficial to the unbanked by giving them a way to transfer money digitally.

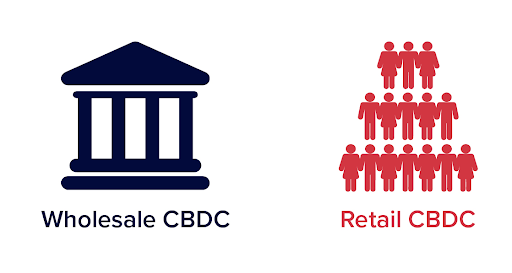

Types of Central Bank Digital Currency – CBDC

CBDCs can fall into different categories. Following are the main types of CBDC are:

Wholesale CBDC

Wholesale CBDCs would be used primarily by financial institutions such as banks. The use of CBDC would allow banks to make payments in a faster and more automated way. Cross-border transactions can become faster and more reliable.

In their current form, payment settlement systems operate in single jurisdictions or with a single currency. The use of blockchain technology could make transactions faster, smoother, and more reliable.

Applications of Wholesale CBDC

Applications of a digital currency issued by central banks based on the wholesale model may also be suitable for international payments. Wholesale CBDCs could help eliminate multiple middlemen and reduce the complexity and cost of cross-border transactions. Furthermore, wholesale CBDCs could also add the value of automation to improve the efficiency of cross-border transactions.

Retail CBDC

Retail CBDCs would be used primarily by individuals. People could essentially use them as digital cash, with the peace of mind of knowing that the currency is issued and backed by the country’s central bank.

This innovation could potentially replace the need to carry physical currency and reduce the economic rents associated with transactions in the legacy financial system.

Applications of Retail CBDCs

Retail CBDCs can find applications in two different variants, such as account-based CBDCs or digital tokens. With the help of deposit accounts in CBDC retail applications, individuals and companies can open accounts with their central bank and receive benefits from similar services offered by commercial banks.

Accounts can help initiate and receive payments as well as view account balances. On the other hand, digital tokens would be electronic replacements for coins and notes. Central banks could issue tokens to commercial banks that have the eligibility to distribute them.

One formidable difference between account-based and token-based retail CBDCs is the need for verification. CBDC accounts would need KYC procedures to verify the accounts of CBDC holders. In the case of CBDC tokens, the process focuses on verifying the authenticity of the tokens and the transaction history.

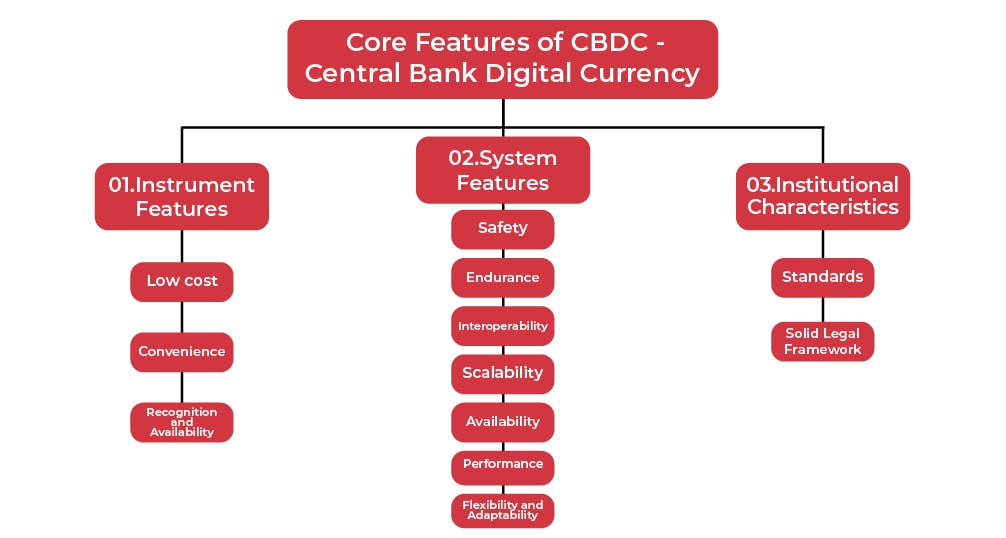

Core Features of CBDC – Central Bank Digital Currency

The role of central bank digital currency features is clearly evident in the fact that they help address fundamental principles. A new CBDC solution would need core features with a specific focus on the instrument itself, the associated system, and the broader institutional framework.

Moreover, one could find instrument features, system features, and institutional features among the main features described for CBDCs. Let’s find out more about the features of each category.

1. Instrument Features

The first edition among the main CBDC features would deal with the features that are specific to the CBDC instrument itself. Some of the main characteristics of the instruments that you can find in CBDC are the following:

- Low cost

Another critical entry among central bank digital currency features concerns the availability of CBDC payments at extremely low or no costs to end users. In addition, CBDC must also ensure the limited technology investment requirement for end users.

- Convenience

CBDC payments should be very convenient and as simple as using cash, scanning a QR code, or swiping a card. With convenient payments, CBDCs could foster accessibility and adoption.

- Recognition and Availability

CBDC should be applicable in all types of transactions that use cash, such as person-to-person or point-of-sale transactions. In addition, CBDC should also offer the ability to transact offline, usually for limited periods and with pre-defined thresholds.

2. System Features

System characteristics are particularly associated with the CBDC system or the platform hosting the solution. The important features of the CBDC system are as follows:

- Safety

The infrastructure, as well as the participants in a CBDC system, must maintain formidable levels of resistance to cyberattacks and other threats. CBDC must ensure effective safeguards against counterfeiting.

- Endurance

Features of central bank digital currencies should also include the facility for increased resilience against operational failures and interruptions due to power outages, natural disasters, or other possible reasons. In addition, end users must also have the ability to make offline payments when network connections are not available.

- Interoperability

The system must have the ability to offer suitable interaction mechanisms alongside private-sector digital payment systems and arrangements to simplify the transfer of funds between systems.

- Scalability

The CBDC system features should have the ability to expand to address the need for potentially large volumes in the future.

- Availability

End users of the CBDC system must have the ability to make payments 24 hours a day, seven days a week, 365 days a year.

- Performance

The CBDC system must have the capacity to process a considerably large number of transactions.

- Flexibility and Adaptability

You should also look for flexibility and adaptability in a CBDC system to ensure it adapts well to changing conditions along with policy imperatives.

3. Institutional Characteristics

The final set of characteristics of central bank digital currencies refers to institutional characteristics. Institutional features actually refer to the general environment in which CBDCs must operate. Notable institutional features related to CBDC are as follows:

- Standards

The CBDC system, including the infrastructure and all participating entities, must comply with all relevant regulatory standards. For example, entities responsible for transferring, storing, or maintaining custody of CBDCs must be held accountable for the regulatory and prudential standards followed by companies that offer the same services in cash or digital money.

- Solid Legal Framework

The central bank must set precedents and clear guidelines to exercise its authority in the process of issuing a CBDC.

Top Use Cases of Central Bank Digital Currency – CBDC

CBDC can be built for wholesale or retail payments. A new infrastructure for interbank settlements is referred to as a wholesale CBDC, whereas a retail CBDC refers to a digital version of cash. Central banks that have been testing CBDCs have been especially focused on fast and low-cost payments.

- Wholesale Central Bank Digital Currency

The purpose of the wholesale CBDC is to make the interbank settlement, i. payments between a few banks and others entities with accounts at the central bank. The daily volume of wholesale CBDCs is typically less than 100,000 transactions.

- Retail Central Bank Digital Currency

Retail CBDC is used for payments between individuals and businesses or other individuals, similar to digital banknotes. Retail CBDC daily volume is typically above 100,000,000 transactions.

What Are the Benefits of Central Bank Digital Currency – CBDC

The central bank’s financial infrastructure currently faces several challenges, from costly payment settlements to declining banknote use to a lack of financial access for citizens far from bank branches.

Studies have estimated that the cost of securities clearing and settlement for central banks in the G7 countries exceeds $50 billion per year, due in large part to the resources required to transfer assets and reconcile accounts.

In addition, today’s cross-border payment systems involve the transfer of assets and sensitive transaction data through several different correspondent banks, exposing institutions and individuals to operational and settlement risks.

Blockchain-based CBDC solves the inefficiencies and vulnerabilities of our current core banking infrastructure by simplifying the creation of a secure payments system that serves as a large-scale decentralized clearinghouse and asset registry.

Benefits of Wholesale CBDC

The following are the benefits of wholesale CBDC:

- Counterparty risk reduction. By enabling payment-versus-payment settlement for transfers in various currencies, CBDC reduces credit risk in cross-border payment transactions.

- Stay ambitious. Although the cost of real-time money transfers has been reduced by centralized platforms like SEPA in Europe, most financial institutions charge customers above cost. CBDC enables end users to benefit from a streamlined banking infrastructure and ensures that central banks maintain a role in interbank settlement amid the broader adoption of stablecoin technology.

- Participate in digital asset markets. As more markets for tokenized assets emerge, there will be a need for tokenized payments. CBDC provides a large-scale decentralized clearinghouse and asset registry to help foster the digital asset revolution.

- Improve the settlement of interbank payments. Through automation and decentralized clearing solutions, CBDC payments are settled instantly between counterparties on individual orders, reducing the risk of overnight batching and collateralization.

Benefits of Retail CBDC

Check out the benefits of retail CBDC:

Promote digital innovation. CBDC’s platform-based software model lowers the barriers to entry for new companies in the payments sector, fostering competition and innovation and pushing financial institutions toward the globalization of services.

Improve monetary policy. CBDC gives central banks direct influence over the money supply, simplifying the distribution of government benefits to the people and improving control over transactions for tax controls.

Increase availability. The digital currency can be distributed on mobile devices, increasing ease of use for citizens who are far from bank branches and cannot access physical cash.

Speed up reconciliation. A CBDC is natively digital and does not require the costly and time-consuming reconciliation currently required for e-commerce and cross-border payments.

CBDC ‘Central Bank Digital Currency’ – Future of Payments

In today’s monetary infrastructure, every citizen has a view of their bank holdings and can transact online by moving/investing funds. However, this digital form of currency is not issued by the Central Bank, therefore all disputes are handled by the Commercial Banks that are involved in the transactions.

- Cryptocurrency

Cryptocurrency is one of the fastest-growing digital currencies running on distributed ledger technology, however, it is not issued by the Central Bank and is highly volatile in nature. Because of this, it is less effective to be used in a financial system that needs stability. To maintain minimal volatility, a stablecoin can be issued that is typically pegged at a 1:1 ratio, based on the value reserved.

- Fungible and Non-fungible Tokens

CBDC can be modeled and distributed as fungible or non-fungible tokens. Fungible tokens make it easy to break tokens and initiate mini-to-micro payments without having a third-party service offering small denominations. While non-fungible tokens do not allow token splitting for payments, adding to a service like a changer can help exchange tokens for smaller denominations. This raises the need for liquidity management to support the change-maker service.

The token ecosystem brings up the concept of digital wallets. A wallet is not the place where the tokens are stored, rather it is a virtual identity of the user that has a key pair corresponding to the address in the ledger that contains the tokens.

- CBDC Wholesale And Retail

CBDCs can be broadly categorized into two types: wholesale and retail CBDCs. While the wholesale CBDC mainly focuses on financial institutes, for example, to hold reserves at the Central Bank, etc., the retail CBDC puts emphasis on consumers and businesses for day-to-day transactions, such as fiat currencies.

Retail CBDC can be further divided based on how people access their coins, i.e. account-based CBDC where they need digital identification or token-based CBDC where a key pair is generated and users can carry out transactions anonymously.

Final Thoughts

Digital currencies issued by central banks, or CBDCs, have the potential to change the way we interact with the digital world. It is crucial to investigate the various applications of this new technology, even though CBDCs are still in their infancy. With a better understanding of how CBDCs can be used, we can imagine a future where these currencies are commonplace.

This blog has provided various use cases associated with wholesale and retail CBDC. CBDCs can help central banks improve the efficiency of their monetary policy operations and payment systems for the time being. They also have the potential to be a more stable value store than traditional fiat currencies. If you have any fintech app development idea, then contact us at Quytech. Our professionals will assist you to the best of their knowledge.