Gone are the days when people used to go to brick-and-mortar financial institutions to transfer, deposit or lend money. Now the focus has shifted to consumer-oriented finance.

People are performing all the financial activities, including investment, lending, wealth management, and portfolio management, on their own with the help of fintech apps.

This way, the role of financial institutions( banks, credit card companies, lending companies, portfolio managers, and wealth managers) is disappearing, and consumers are performing all the financial chores without the need for any middlemen.

This significant change in the financial world is known as the consumerization of institutional finance. Some leading factors contributing to the growth of the change are the growing rivalry between traditional competitors and the rise of disruptive fintech players like PayPal and Google Wallet.

This growing trend has also shown a ray of hope for fintech startups looking to establish themselves in the financial world. However, financial startups need a thorough understanding of their customers to provide them with relevant and tailored products and services.

So, in this blog today, we will discuss in detail the consumerization of financial institutions, the rising benefit for fintech startups, and how people are going to use fintech products seamlessly.

Let’s begin!

How Are Consumers Interacting with Financial Institutions?

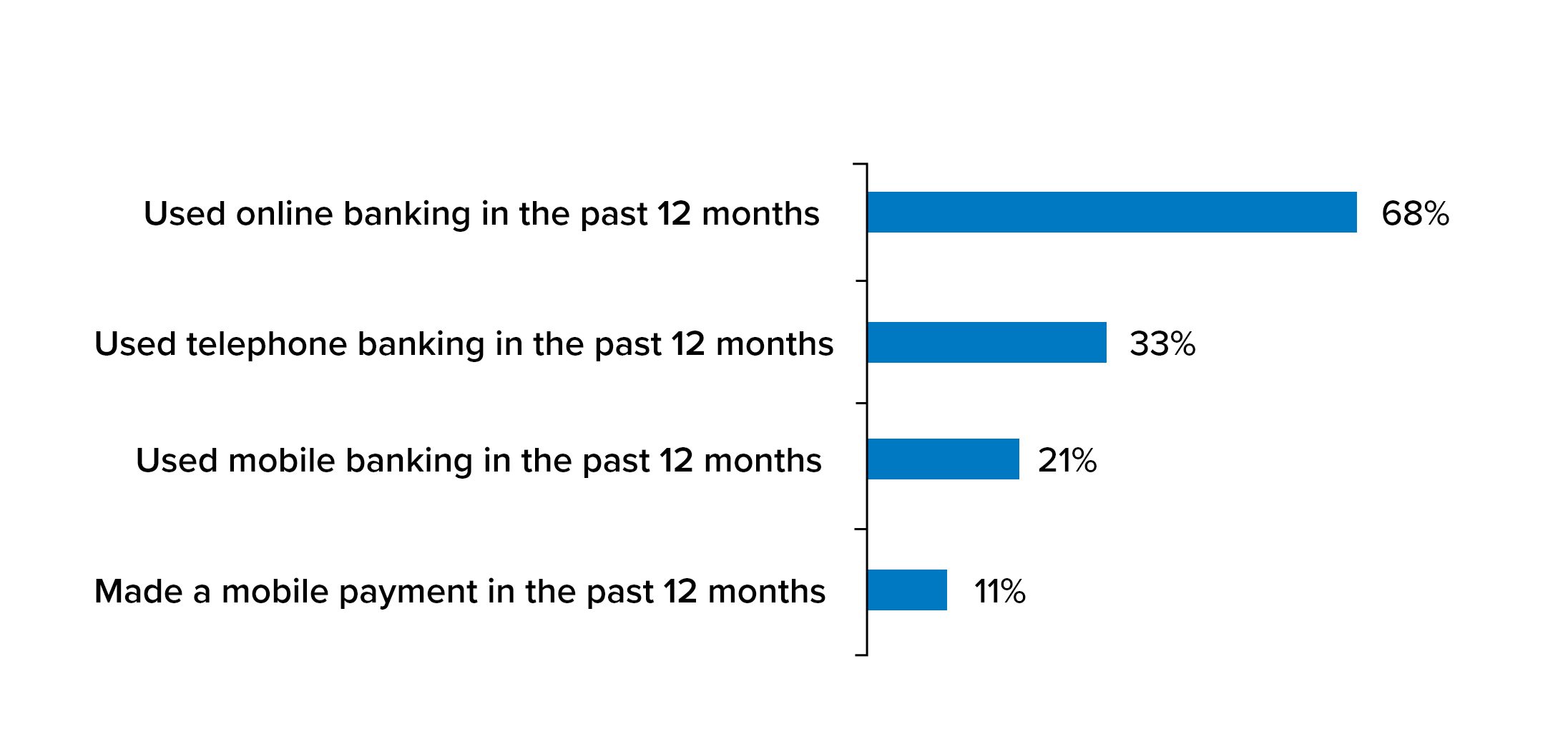

Before diving deeper, let’s first understand how US consumers interact with financial institutions. A survey was conducted among respondents, who answered questions about whether they had a bank account, access to a stable internet connection, and their smartphones.

Based on survey responses, it appears that many Americans interact with their financial institutions using some form of technology.

For example, as depicted in the figure below, 68% of respondents said they used online banking in the past 12 months. 33% of respondents said they used telephone banking, And 21% reported using mobile banking during the same period.

Having said that, it shows people are moving towards financial technology-driven services.

Also Read- Use Cases of AI in the Fintech Industry

How Fintech Startups Can Reduce Friction And Drive Value

Frictionless finance isn’t just an alliterative phrase. It represents a new way of thinking about payments by leveraging incremental information to make the payment process smoother and create greater value for customers.

Frictionless finance also refers to the easy lending of money without doing any paperwork and getting the lending amount within hours.

Fintech startups can employ financial technologies and offer customers tailored financial services like investment, money lending, and portfolio management at their fingertips. Consumerization of institution finance has the caliber to reduce friction and drive more value with the help of fintech solutions.

Let’s see how the rise of online banking, mobile banking, digital currencies, and Robo-advisors paved the way for the consumerization of institutional finance.

1. The Rise of Online Banking

Banking used to be something that was primarily done at a branch, but now more and more people are banking from the comfort of their own homes. Banking online has become so popular that brick-and-mortar locations are closing down or converting into community banks.

It seems that this new trend in banking stems from a desire for institutions to cater their services to consumers rather than the other way around. These institutions can get customers hooked on their service by offering free checking accounts and credit cards with no annual fee. In return, these customers stay loyal to the institution.

2. The Rise of Mobile Banking

The rise of mobile banking made financial services more accessible to the average user and let people do things on their own schedule. With mobile banking, people don’t need to take time out of their day to go into a bank branch to do transactions such as depositing checks or transferring funds.

All they need is a stable internet connection, and they’re good to go. Mobile banking has been a boon for not only customers but also the banks themselves, who are seeing significant increases in deposits through these channels. With all this interest from consumers and increased productivity from banks, we see this trend continuing in the years ahead.

3. The Rise of Digital Currencies

Digital currencies have been on the rise in recent years, and they are poised to become a significant player in the institutional finance world. Digital currencies allow for peer-to-peer transactions without any third-party involvement, which eliminates the overhead and fees associated with traditional financial institutions.

In addition, digital currency transactions cannot be reversed by the sender, which reduces both fraud and the risk of chargeback disputes from clients. This means that merchants will see better conversion rates as customers are less likely to dispute charges made with digital currencies.

Also Read- How to Develop Peer-To-Peer Payment App?

4. The Rise of Robo-advisors

There has been a significant rise in the number of Robo-advisors in recent years, which have been increasingly embraced by consumers and professionals alike. Consequently, the process of buying and selling stocks has changed dramatically over the last few years. You can now invest in a variety of assets without having to pay a large commission for doing so.

Consumerization Expedited The Growth of Fintech Apps

Having discussed how the consumerization of institutional finance is driving value, let’s see how it has expedited the growth of fintech apps like alternative investment apps, portfolio management apps, crypto trading apps, P2P lending apps, and several fintech apps that you can develop for your startup.

1. Alternative Investment Apps

Alternative investment apps have grown tremendously in popularity in recent years due to their potential for providing greater returns than traditional investments such as stocks and bonds. People can now invest in alternative investments through the alternative app without the help of any financial institutions. This has proved to be fruitful for fintech startups and users alike.

2. Portfolio Management Apps

People are now more tech-friendly than in the past and rely on portfolio management apps to manage all their investments in a place. They don’t require a portfolio manager anymore to help them manage their investments. People can instantly and conveniently see the investments through the portfolio management app, along with tracking the result.

3. Wealth Management Apps

Instead of relying on financial institutions like banks, consumers like to use wealth management apps as the apps provide all the essential benefits to the users. Consumers can easily track their spending, pay the bills conveniently, and get advice on financial planning.

This way, they don’t need to visit financial institutions to track transactions or perform money transfers. This is all possible now with the help of wealth management apps.

4. Peer-to-Peer Lending Apps

Consumerization of institutional finance has also led to the rise of peer-to-peer lending, which provides an alternative financing option for people to get a loan by downloading P2P apps.

Companies such as Lending Club and Prosper have been able to give consumers another option by connecting them with investors who are willing to lend money at rates that are typically lower than those charged by banks or credit unions.

In turn, this allows borrowers to pay back the loans over time rather than paying it all off immediately. The benefits don’t end there; these companies also offer services to help their customers manage their finances better.

For example, both Lending Club and Prosper offer budgeting tools so borrowers can track their spending habits over time to make sure they’re on track to repay their loans.

They also offer advice on how much debt each borrower should carry based on several factors, such as age, income, and monthly expenses.

5. Stock Trading Apps

Earlier, when people wanted to buy or sell stocks, they had to contact brokers. Now it is not the same story anymore. People can now sell or buy stocks with the help of stock trading apps and earn money. They can easily monitor the flow of funds through the app, and all confidential information remains safe and secure.

Also Read- How to Build a Stock Trading Apps like Robinhood?

Concluding Lines

We are going to witness more depth in the consumerization of institutional finance with the advent of new financial technologies in the next few years. Financial institutions’ roles are diminishing day by day since the rise of new fintech apps in the markets that offer value-driven services to consumers.

People are now able to perform almost all financial activities without visiting financial institutions, increasing efficiency and getting more consumer-centric services through the comfort of their homes or offices. They can transfer, lend, and invest money with the help of fintech apps without the need for intermediaries.

If you are a startup or an entrepreneur looking to develop fintech apps, it’s high time to do so. You can establish your name in the financial sector by developing P2P lending apps, alternative investment apps, stock trading apps, or portfolio management apps for the millennials.

So why delay now? Contact us at info@quytech.com and discuss with us your innovative idea to create user-friendly fintech solutions.